Financial Loan Analysis 2021

Table of Contents

- Project brief

- Questions

- Data source

- Tools

- Stages

- Chart types and why

- Processing

- Dashboards

- Data Transformation

- Findings

- Recommendations

Project brief

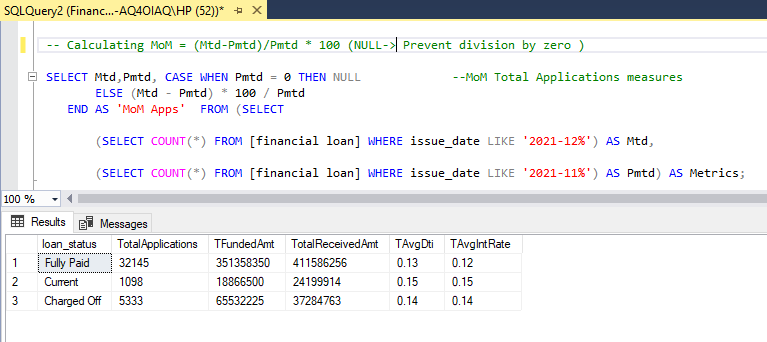

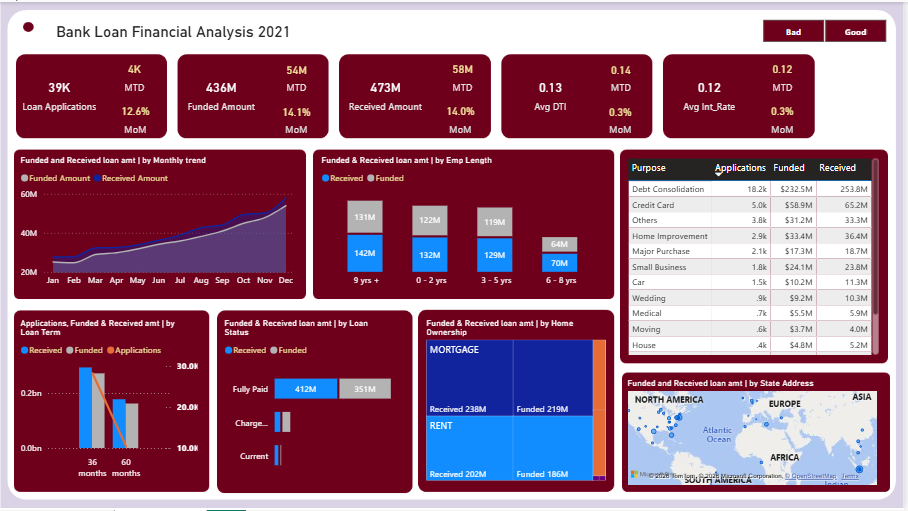

The dashboard provides a detailed breakdown experience, allowing stakeholders to identify not just what happened, but why it happened by comparing Month to Date (MTD) performance against the Month over Month (MoM).

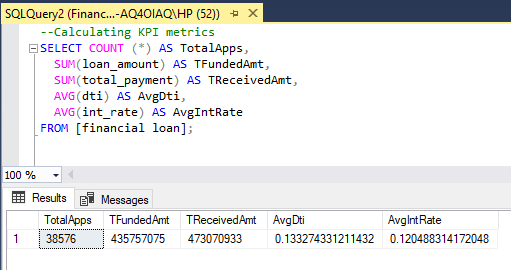

Developed a comprehensive Bank Loan Intelligence System that analyzes over $435M in loan data to monitor portfolio health and borrower risk. By visualizing key metrics like a 13.3% average DTI and identifying Debt Consolidation as the primary loan driver, this project provides actionable insights to improve lending strategies and maintain a 86.2% Good Loan rate.

Questions

-

How is the overall loan portfolio performing? (Answered by the 86.2% Good Loan vs. 13.8% Bad Loan split).

-

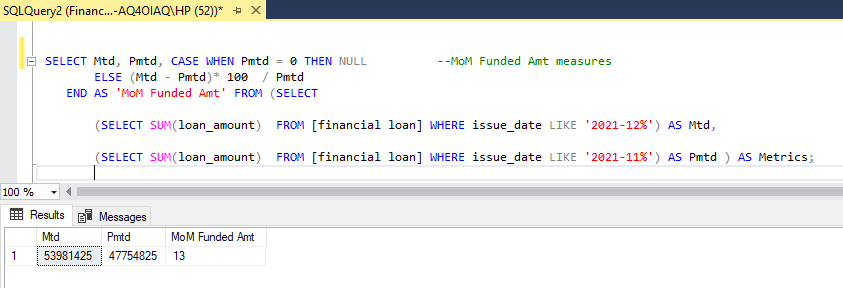

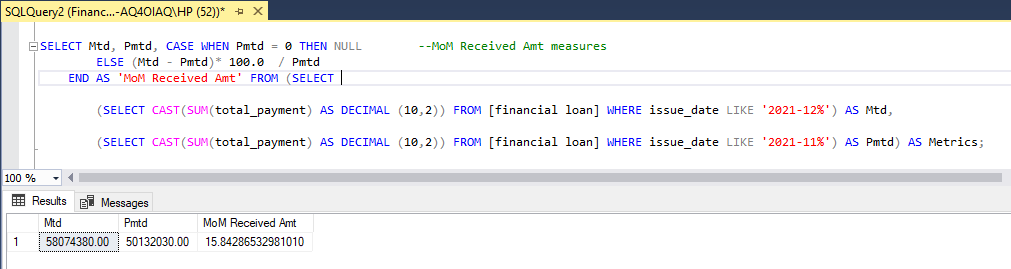

What is the total financial exposure and recovery status? (Answered by the $435.8M Funded Amount vs. the $473.1M Total Amount Received).

-

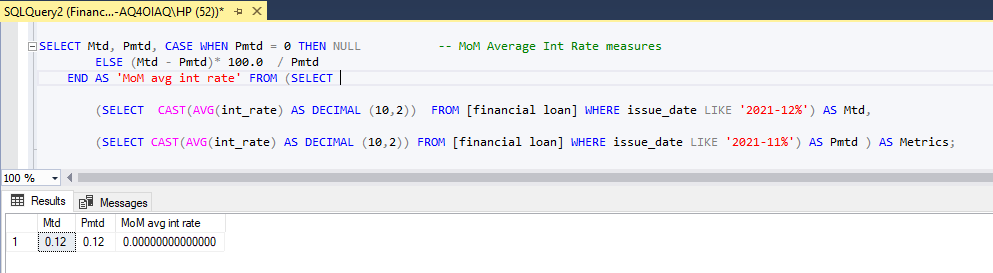

Are we maintaining a healthy profit margin? (Answered by the 12.0% Average Interest Rate compared to the volume of funded loans).

-

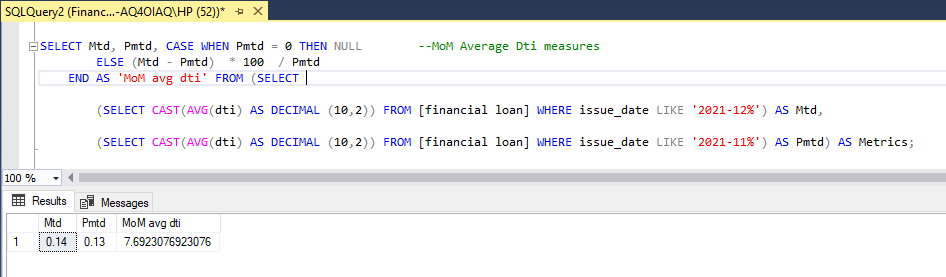

What is the average financial burden on our borrowers? (Answered by the 13.3% Average Debt-to-Income (DTI) ratio).

-

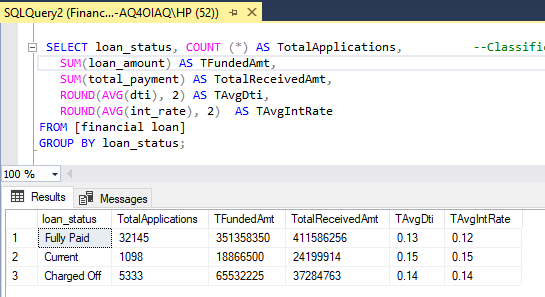

Which loan types are most likely to fail? (Answered by the “Bad Loan” breakdown in the Summary dashboard).

-

Are longer-term loans riskier than shorter ones? (Answered by the Term breakdown—36 months vs. 60 months—on the Overview page).

-

What is our “ideal” customer profile? (Answered by the Employment Length and Home Ownership charts).

-

What are the primary drivers for people seeking credit? (Answered by the “Loan Purpose” chart, e.g., Debt Consolidation).

-

Does job stability correlate with loan volume? (Answered by the breakdown of applications from people with 10+ years of work history).

-

Is the demand for loans growing or shrinking? (Answered by the “Total Loan Applications by Month” line chart).

-

Where is our business geographically concentrated? (Answered by the “Loan Applications by State” map).

-

Are we seeing a month-over-month (MoM) improvement in collections? (Answered by the MoM percentage indicators on the Summary cards).

-

Which specific individuals or accounts require immediate follow-up? (Answered by the Details table, allowing managers to see specific loan statuses and payment dates).

-

How are different grades of loans (A, B, C, etc.) performing across the board? (Answered by the Grade and Sub-Grade filters in the detailed report).

Data Source

Tools

| Tools | Purpose |

|---|---|

| SQL, Power BI | DAX, Power Query |

Stages

-

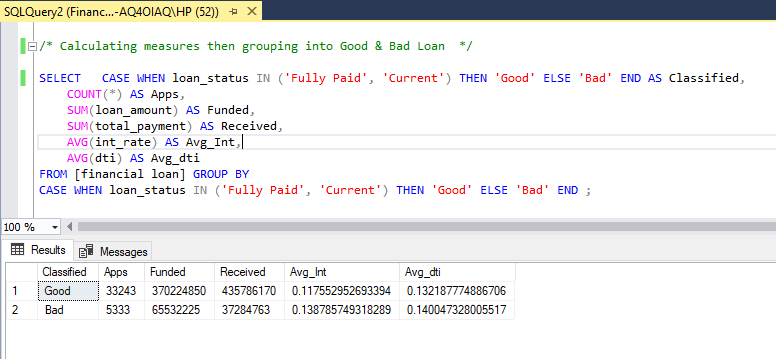

Import cleaned and process data in SQL.

-

Export processed data from SQL to PowerBI (power query) for Interactive and dynamic visualization.

-

Modeled data to; (1) Improves query performance and report responsiveness. (2) Simplifies DAX logic by enforcing a single-direction filter flow.

(3) Ensures accurate time-intelligence calculations. (4) It follows industry best practices for Power BI solutions.

-

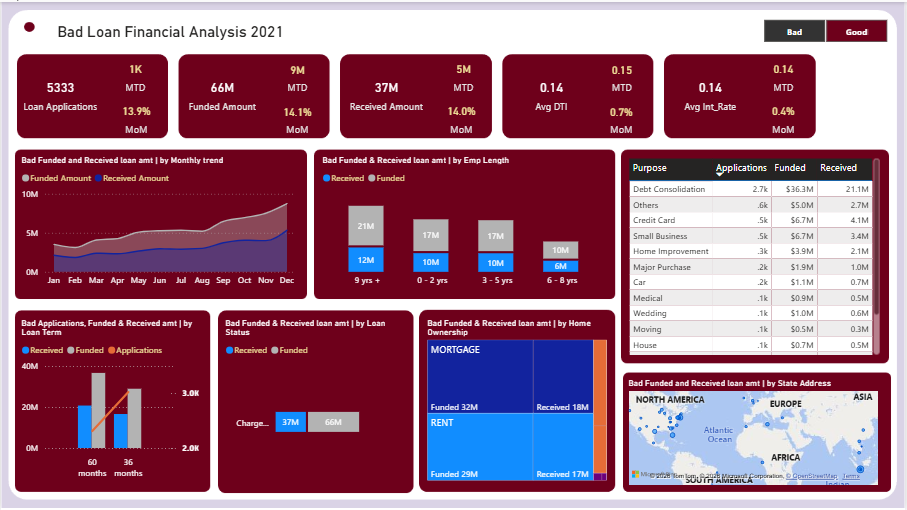

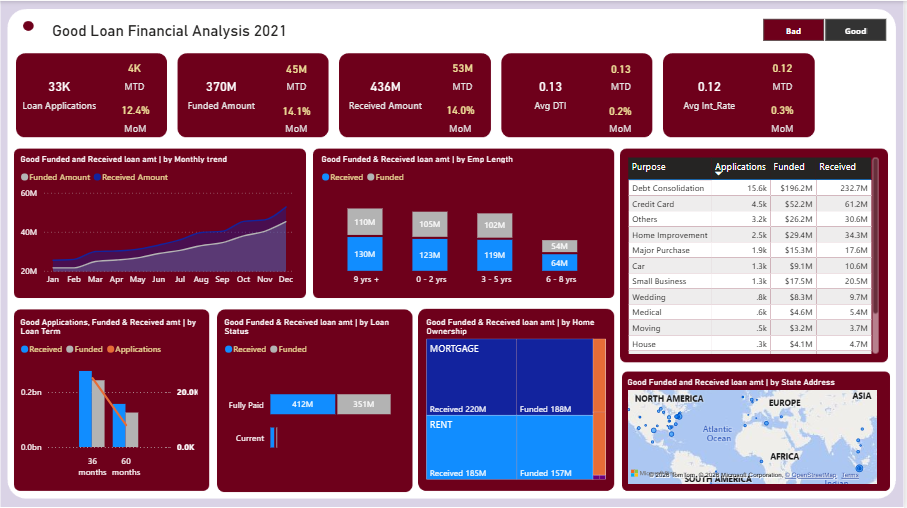

Create a custom ‘slicer’ as a toggle button to view across 2 pillars of business. (Good and Bad Loans), and to return “All” if slicer is cleared.

-

Wrote DAX measures to calculate for Dynamic report.

Chart types and Why?

-

Card Visuals - Shows the KPIs metrics (Applications, Funded and Received amount, Avg DTI and Int Rate, MTD & MoM), and also the dynamic report title.

-

Table Charts - Shows the application, funded and received by loan purpose.

-

Treemap - Shows the application, funded and received loans by home ownership.

-

Map - Used to depict the geo location of loan borrowers / applicants.

-

Column Bar (Combo) - Shows the categorical distribution of loans by employment length.

-

Bar - It display the categorical distribution of loan status between Charged off (Bad), Current and Fully Paid (Good).

-

Line - It is used to show the monthly trends of applications, funded, and received amount.

Processing - SQL.

Dashboard

This dashboard allows the Sales Director to pivot from ‘General Observation’ to ‘Targeted Action’ for example, specifically investigating the November slump or renegotiating low-margin accounts identified in the scatter plot.

Data Transformation

Here are the Key DAX formulas used in this project:

-

Applications = VAR FilterState = [Loan Quality_Filter] RETURN CALCULATE( COUNT(financial_loan[Id]), FILTER( financial_loan, FilterState = 0 || (FilterState = 1 && financial_loan[Loan Quality] = “Good”) || (FilterState = 2 && financial_loan[Loan Quality] = “Bad”) ) )

- This measure count all loans applications.

-

Funded = VAR FilterState = [Loan Quality_Filter] RETURN CALCULATE( SUM(financial_loan[Loan_Amount]), FILTER( financial_loan, FilterState = 0 || (FilterState = 1 && financial_loan[Loan Quality] = “Good”) || (FilterState = 2 && financial_loan[Loan Quality] = “Bad”) ) )

- This measure total all funded amount.

-

Received = VAR FilterState = [Loan Quality_Filter] RETURN CALCULATE( SUM(financial_loan[Total_Payment]), FILTER( financial_loan, FilterState = 0 || (FilterState = 1 && financial_loan[Loan Quality] = “Good”) || (FilterState = 2 && financial_loan[Loan Quality] = “Bad”) ) )

- This measure sums the payment from loan borrowers.

-

Avg Int = VAR FilterState = [Loan Quality_Filter] RETURN CALCULATE( AVERAGE(financial_loan[Int_Rate]), FILTER( financial_loan, FilterState = 0 || (FilterState = 1 && financial_loan[Loan Quality] = “Good”) || (FilterState = 2 && financial_loan[Loan Quality] = “Bad”) ) )

- This measure is used to calculate the AVG Int Rate

-

Avg DTI = VAR FilterState = [Loan Quality_Filter] RETURN CALCULATE( AVERAGE(financial_loan[DTI]), FILTER( financial_loan, FilterState = 0 || (FilterState = 1 && financial_loan[Loan Quality] = “Good”) || (FilterState = 2 && financial_loan[Loan Quality] = “Bad”) ) )

- This measure is used to calculate the AVG DTI

Findings

-

86.2% of all loans are “Good Loans” (Fully Paid or Current), totaling $370.2M in funded value.

-

Most borrowers are highly stable, with 10+ years of employment history and living in rented or mortgaged homes.

-

Debt Consolidation is by far the most common reason people apply for loans, followed by Credit Card payments.

-

There is a clear upward trend in loan applications from the start of the year toward the end (peaking in December).

-

About 13.8% of loans are “Bad Loans” (Charged Off), which represents roughly $65.5M in total funded amount.

Recommendations

-

Create marketing campaigns specifically for employees with 10+ years of experience, as they are your most active and reliable customers.

-

Since this is the #1 loan purpose, offer a streamlined “Express” approval process for debt consolidation to capture more market share.

-

Focus marketing spend on California (CA), Texas (TX), and New York (NY), as these states show the highest demand and volume.

-

Investigate the “60-month” loan terms more closely; longer terms often carry higher risks. Consider stricter credit requirements for 5-year loans.